With

the Federal Reserve pondering how they can unscrew themselves from the corner that their experiments have screwed them quite firmly into (i.e Operation Twist), I thought it was time to look at a paper by James Bullard,

President and CEO of the Federal Reserve Bank of St. Louis. This paper,

entitled "Seven Faces of "The Peril" (a rather ominous sounding

title, don't you think?) was released in late July 2010 and looks at the

deflationary issues facing Japan's economy and how the actions taken by the

Federal Reserve’s Federal Open Market Committee (FOMC) could help avoid this

economic nightmare (for central bankers) with their program of quantitative

easing or how they could mimic Japan’s problem by implementing a long period of

near zero interest rates. Let's delve more deeply than we ever have into

the mind of a central banker.

Mr.

Bullard opens with the rather frightening "...most worrisomely, current

monetary policies in the U.S. (and possibly Europe as well) appear to be poised to head

straight toward the problematic outcome described in the paper.". The paper he refers to

was written by three academic economists in 2001 and is entitled "The

Perils of Taylor Rules". For those of you who aren't aware of

Taylor-type economic policy, it occurs when central bankers change nominal

interest rates at a more than one-for-one ratio when inflation deviates from a

given target. Taylor Rules are basically a guideline for interest rate

manipulation where changes in interest rates are used to both stabilize the

economy in the short-term and maintain long-term growth. Central banks

will raise interest rates in times of high inflation and lower rates when

inflation is low. In general, Taylor Rules are followed by many of the

world's central banks today on either a formal or informal basis. As

well, in the “Perils of Taylor” paper, the authors emphasize that a combination

of Taylor Rules and a zero limit on interest rates will create a new outcome

for a given economy that will result in very low interest rates and a

deflationary environment. One need look no further than Japan to see

Taylor rules and deflation in action as we will see.

To

open, and for your information, here are two graphs showing the benchmark

interest rates for the United States and Japan since the very early 1970s:

Notice

that while Japan’s benchmark rate has been low since the mid-1990s, the U.S.

interest rate pattern is quite similar and could well replicate what has been

experienced in Japan.

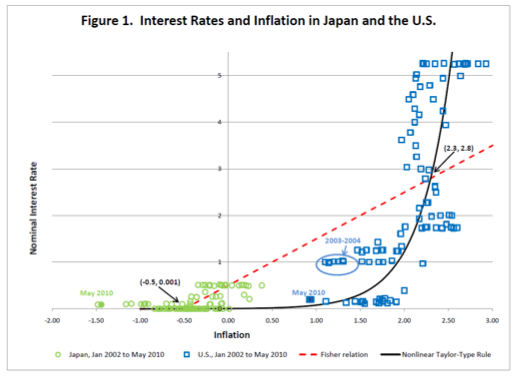

Now

let's look at a graph from Mr. Bullard’s research showing both monthly

short-term interest rates and inflation for Japan (round green data points) and

the United States (square blue data points) from 2002 to 2010 with inflation on

the horizontal axis (with the negative numbers showing deflation) and nominal

interest rates on the vertical axis:

Please bear with me while I attempt to explain what this graph is telling us. The

red dashed line is called the Fisher relation or Fisher hypothesis. In

the Fisher hypothesis, the real interest rate is equal to the nominal interest

rate (the rate you see posted at your local bank for example) minus the expected rate of

inflation. In this case, Mr. Bullard has taken the real component of the

interest rate and fixed it at one-half percent or 50 basis points. In

Main Street speak, if nominal interest rates are 1 percent, then the Fisher

relation will bring real interest rates up to 1.0 plus 0.5 or 1.5 percent.

Looking at the curved black line, we see the Taylor Rule in action.

This line describes what central bankers do as inflation rises, that is,

they raise interest rates. When inflation is above their preferred

target, they raise interest rates at a more than one-for-one ratio. When

inflation is below their preferred target, central bankers raise interest rates

at less than a one-for-one basis. Notice on the graph that the straight

red line (the Fisher line for lack of a better label) crosses the curved black

line. This is called the steady state where the central bank no longer

wishes to raise or lower interest rates. This is the point where central bankers have to raise

interest rates at more than the rate of inflation, that is, where inflation is

greater than 2.3 percent and nominal interest rates are greater than 2.8

percent, interest rate increases are greater than one-to-one. Thus, the

black line becomes steeper because it takes greater increases in interest rates

to keep inflation within the central bank's target zone.

Now,

if you look at the far left side of the graph, you'll notice that the red

dashed line and black curved line intersect once again in amongst the green

Japanese circles. This second or unintended low interest rate steady

state occurs where inflation (or in this case, deflation) is negative one-half

percent (-50 basis points) and interest rates are nearly zero. In this

case, the policy rate cannot be lowered below zero but it is not really

necessary (or possible for that matter) since inflation is non-existent. That's

most fortunate since the Bank of Japan has absolutely no "wiggle

room" left. Unfortunately, deflation is the stuff made of

nightmares for central bankers and is exactly the outcome that they do not want

from messing with interest rates.

Central bankers, particularly the Fed, are trying desperately to avoid

ending up with the blue squares representing the U.S. experience with inflation

and interest rates overlying the area on the graph covered with little green

circles.

Note

that the little solid coloured blue data point labeled "May 2010"

lies very close to the horizontal axis of the graph along with a whole

collection of other similar data points. These data points are showing us

that American interest rates are nearly zero but that there is still inflation

within the system, unlike in the case of Japan. The "May 2010"

point does, however, show a potential slide toward the Japanese model discussed

above. With the Federal Reserve recently announcing that it was

committing to a long-term policy of near zero rates, it would appear that they

have boxed themselves into a corner. The Fed wants and needs at least

some level of inflation but, from the example of Japan's green data points, we

can see that the ultimate outcome of extremely low interest rates could be the

much dreaded negative inflation. Here's a quote from Mr. Bullard's paper:

"Both

policymakers (the world's central bankers) and private sector players continue

to communicate in terms of interest rate adjustment as the main tool for the

implementation of monetary policy. This is increasing the risk of a

Japanese-style outcome for the U.S."

What

he's saying is that the use of interest rates as a means to control the level

of inflation (i.e. Taylor Rules) by central bankers around the world do not always

work. Deflation can and may well occur because of the Federal Reserve's

long-term pledge to keep interest rates at a near zero level.

Through

the remainder of the article, Mr. Bullard goes on to suggest that divisions

among economists about his findings range from denial to tinkering with the

minimum interest rate level that should be allowed. He also discusses the

policy of quantitative easing and how it is expected (hoped) to be

inflationary. Here's a quote:

"...The

experience in the U.K. seems to suggest that appropriately

state contingent purchases of Treasury securities are a good tool to use

when inflation and inflation expectations are too low. Not that one

would want to overdo it, mind you, as such measures should only be undertaken

in an effort to move inflation closer to target." (my bold)

One

question: how do central bankers know when they have overdone quantitative

easing? Is it possible that QE 3,

if implemented, could be the straw that breaks the camel’s back?

Basically,

those of us who live on Main Street are the subjects of a gigantic fiscal

experiment by central bankers, most particularly the Federal Reserve.

They have no precedent which will allow them to predict the long-term

outcome of their policy of ultra-low interest rates other than Japan and that

is exactly the outcome they desperately need to avoid. Interestingly

enough, according to the Bank of England, in 314 years, interest rates never

fell below 2.0 percent until recently.

That is most telling.

Here

are Mr. Bullard's concluding remarks:

"The

global economy continues to recover from the very sharp recession of 2008 and

2009. During the recovery, the U.S. economy is susceptible to negative shocks

which may dampen inflation expectations. This could possibly push the

economy into an unintended, low nominal interest rate steady state. Escape from

such an outcome is problematic. Of course, we can hope that we do not

encounter such shocks, and that further recovery turns out to be robust but

hope is not a strategy. The U.S. is closer to a Japanese-style outcome today than at any

time in recent history."

(my bold)

The recent debt issues facing the Eurozone make it less and

less likely that the world will return to a normal interest rate environment

anytime soon. Inflation, as shown on the graph at the beginning of this

posting can move one of two ways. Should it move toward the green

circles, the United States could well experience Japan's "lost

decade".

Remember this rule of thumb: economics is not a science,

rather, it’s more akin to medieval alchemy. The actions of today’s central bankers are all the proof

that we need.

Interesting information. I enjoy the opportunity to educate myself futher about economics. (I had three economics courses in college, which is barely enough to scratch the surface of the subject.)

ReplyDeleteThe curves show some correlation, but as I'm sure you know, correlation does not prove causation. The underlying reasons for Japan's lost decade (and potentially our own) is way more involved than just low interest rates. We can't raise interest rates if the economy is weak and there is little inflation, now can we? Wasn't that one of the big mistakes made during the Great Depression - which I think we can call, GD1?

Thanks,

Lou www.the-moderates-perspective.blogspot.com

I'm a bit late (like 4 months) to this conversation, the link was referred in a WSJ article comment. The question is are the low interest rates the cause or the consequence of deflation. I would tend towards the latter. To understand deflation, one needs to look at multiple factors. In Japan is demographics - older citizens are a higher percentage of the populace than in any other western country, and these guys have no inclination for shopping sprees. In the US is globalization: a large open economy is allowing competition from firms in Asia.

DeleteEurope is different: even with 20% jobless rates, a country like Spain manages to have inflation north of 3%. UK is in a technical recession, but inflation is alive and well. Why is that? These economies, while pretending to be open, have many non-tariff barriers to external competition - from benign things like language based restrictions to more aggressive local regulations that give entrenched incumbents an edge over newcomers. Germany is the one exception, but who knows for how long?

So the sequence of events in Japan was: deflation begets low interest rates, not the other way around.

Interest rates on sovereign debt, in large part, depend on market forces rather than what central bankers really want or desire. Just ask Greece, Italy, Spain.....

ReplyDeleteA very fundamental premise of economics is that markets/prices will move toward equalization between supply and demand, correct? (I know it's over simplified, but it's still a valid concept.) So as you say, interest rates depend on market forces to a great degree. Governments set rates for banks, and they manage the money supply - by putting money into (or taking money out of ) circulation) so it's not completely market driven. I mean, let's face it: without government created and managed currency, there would be no currency. Some people talk about governments printing money like it is some evil thing - and money is somehow otherwise created by nature. :) But, it's all created by government; it has to be. So it's never going to be perfect. Isn't currency just a mechanism for distributing value and productivity? That's why I don't believe the dollar should be "backed" by gold, (or any other tangible thing). Gold is no more viable in terms of a currency mechanism than anything else. For example, it could be possible in the future that all currency will be in electronic form. How could you ever back that with gold?

ReplyDelete