Updated May 2016

Consumer debt levels are becoming increasingly worrisome, an observation that is not terribly surprising given the long-term impact of the Fed's ultra-low interest rate policy that is specifically designed to get consumers to spend, spend spend.

Consumer debt levels are becoming increasingly worrisome, an observation that is not terribly surprising given the long-term impact of the Fed's ultra-low interest rate policy that is specifically designed to get consumers to spend, spend spend.

Let's start by looking at

what has happened to overall household debt levels as of March 31, 2016 from the

New York Federal Reserve Bank:

At the end of Q1 2016,

non-housing debt (in pink) reached $3.4 trillion on top of $8.85 trillion in housing

debt (in blue). While overall household debt is 3.3 percent below its peak of

$12.68 trillion in Q3 2008, non-housing debt is now at the highest level

that it has been since Q1 2004. In fact, non-housing debt peaked at

$2.71 trillion in Q4 2008 during the Great Recession and dropped to a

post-Great Recession low of $2.56 trillion in Q2 2010. Since its low in

2010, non-housing debt has risen by $840 billion or 32.8 percent.

Let's focus on

non-housing debt and then take a closer look at credit card debt. Here is a graph from the Philadelphia Federal

Reserve showing how total revolving and non-revolving consumer credit has

reached a 24 year high:

In the first quarter of

2015 (the latest data available), total outstanding consumer credit reached $3.364 trillion which is

composed of $890.9 billion in revolving credit and $2.473 trillion in non-revolving

debt. This is up $811.9 billion or 31.8 percent from the Great

Recession low of $2.552 trillion in 2009.

According to Tim Chen at

Nerdwallet and based on an analysis of Federal Reserve statistics, an average

American household had the following consumer debt in July 2015:

Credit card debt: $7400

Mortgage debt: $156,584

Student Loan debt:

$33,090

If the households that

have no credit card debt are removed from the equation, the average outstanding

credit card debt more than doubles to $15,863.

As we can see on this

graph, the number of credit card accounts (in blue) has risen to its highest

level since the Great Recession:

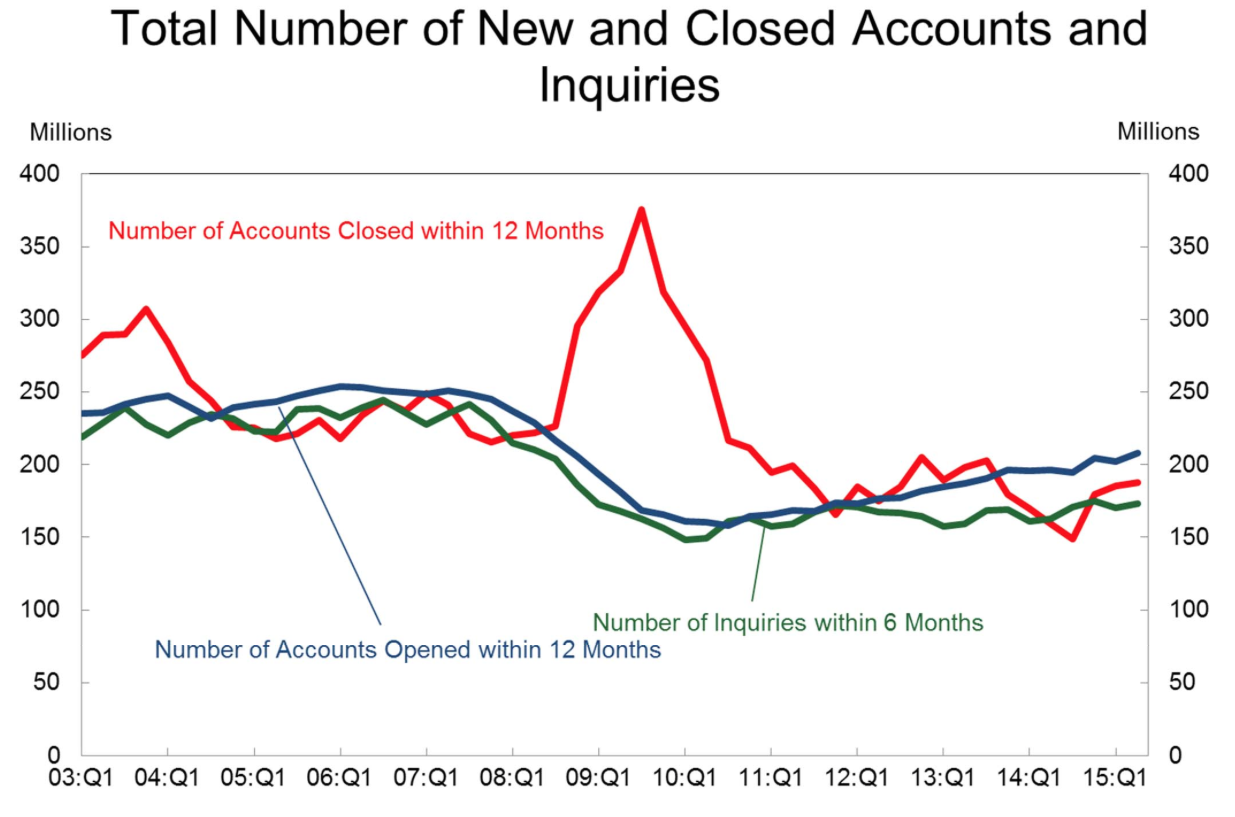

As well, the number of

credit accounts opened (in blue) and number of credit inquiries (in green) have

risen to or just below new post-Great Recession highs:

Over the second quarter,

the number of credit inquiries rose by 3 million to 173 million. This is

a key indicator of consumer non-housing credit demand and would suggest that consumers are feeling rather confident.

In the second quarter of

2015, credit card balances increased to $703 billion with 8.4 percent of

balances delinquent by 90 days or longer. Here is a graph showing how the

percentage of credit card delinquent balances (in blue) have begun to rise over

the last two quarters:

While the level of

delinquencies is still well below the levels seen in early 2010, as Tim Chen

points out, credit card indebtedness and delinquency levels are connected to a

significant increase in credit card companies who continue to write-off

(charge-off) seriously delinquent credit card debts.

It is interesting to see

how consumer debt, particularly credit card debt, has reached post-Great

Recession highs and how consumer credit inquiries are up. It appears that

the current and prolonged low interest rate environment has lulled consumers

into a false sense of credit reality. As we can see on this graph from FRED, the current average

interest rate of 12.31 percent on commercial bank credit cards is among the

lowest in the last two plus decades:

It will be interesting to

see how quickly consumer credit delinquency rates begin to rise once the Federal Reserve begins

to normalize its monetary policies if, indeed, it does.

A great deal of our economic system is about debt. It is important to remember not all debt is created equal. A mirage is a naturally occurring optical phenomenon in which light rays are bent to produce a displaced image of distant objects. Joining the idea of a mirage and contagion with the reality of collapsing debt forms an interesting subject.

ReplyDeleteIt is important to remember all debts and obligations do not come due at the same time. Also, it must be noted when a bill is not paid or defaults it often starts a long and drawn out legal battle, this collection process that may extend years without harsh consequences. This my friends is the reality of modern life in America and much of the world. More about debt in the article below.

http://brucewilds.blogspot.com/2014/05/debt-mirage-always-moving-into-distance.html