The markets have been all gaga about

the recent data coming out of America's manufacturing sector. The Federal Reserve's data release showed that

factory production climbed and that capacity utilization (the amount that a

factory is in use) increased to levels not seen since June 2008. Capacity

growth rose by 1.8 percentage points on a year-over-year basis, hitting 79

percent in November 2013. While this is definitely an improvement over

the 2009 low of 66.9 percent, is is not particularly outstanding when taken

into historical perspective as shown here:

Capacity is still nearly 1.5

percentage points lower than it was between February 2007 and February 2008 and

is well below the 83 percent plus range experienced between 1994 and 1998.

It is particularly mediocre when compared to the 87 percent plus range

seen in the late 1960s and early to mid-1970s when America was a manufacturing

behemoth. As well, the current capacity utilization is still down 1.2

percentage points from the 1972 to 2012 average of 80.2 percent and is just

above the 78.8 percent nadir experienced during and after the 1991 - 1992

recession.

While some "experts" are

touting this newfound growth in manufacturing as a harbinger of good things to

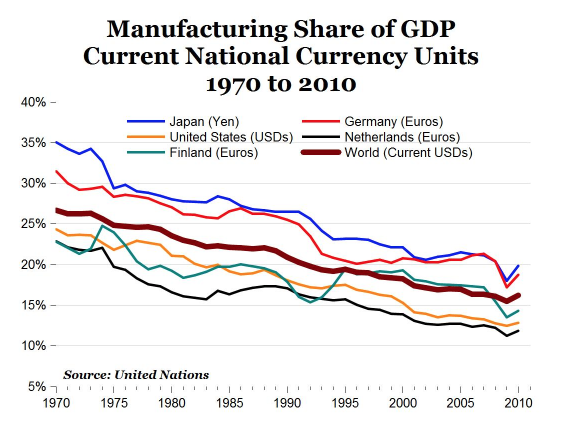

come from the Federal Reserve, as you can see on this chart, manufacturing is a

far less important part of the American economy than just about any time in the

last forty years:

In 1970, manufacturing in the United

States made up 24.3 percent of the total economy and fell to 12 percent in

2011. This follows a global trend that has seen the world's manufacturing

share of GDP in advanced nations fall from 26.6 percent in 1970 to 16.2 percent

in 2010.

The United States Chamber of Commerce seems to feel that this is

a good thing and that it merely reflects the shift from a manufacturing

intensive "Machine Age" economy to a modern, service-intensive

"Information Age" economy. A study from the Information Technology and

Innovation Foundation (ITIF) suggests otherwise.

The authors of the ITIF study

show that between 2000 and 2010, America lost 5.7 million manufacturing jobs or

33.1 percent of the total. These manufacturing job losses compare to the

loss of 30.9 percent of manufacturing jobs between 1929 and 1933. Here is

a graph showing the percentage of job losses for each industrial group within

the manufacturing sector between 200 and 2010:

The percentage of jobs lost in the

manufacturing sector during the latest recession were the worst since the

Second World War as shown on this graph:

Here is a map showing the

percentage loss in manufacturing jobs by state for the period from 2000 to

2010:

As well, while the overall change in

real manufacturing value-added appears to be growing relative to GDP as shown here:

...many industries are showing

output declines with 13 of the 19 sectors that employ 55 percent of

manufacturing employees producing less in 2010 than they were in 2000.

Largely, the authors feel that output growth in both the computer and

electronic and the petroleum and coal sector being overstated, making the manufacturing sector appear much healthier

than it is.

The authors note that, while

productivity increases were partially responsible for declining employment in

the manufacturing sector, the overriding factor was the decline in output.

If manufacturing output had grown by the same rate as the rest of the

business sector between 2000 and 2010, the United States would have 3.8 million

more manufacturing jobs than it currently does.

Here is a graph showing the

percentage change in manufacturing real value by industrial group

for the period from 2000 to 2010:

Notice that the lion's share of

growth is in two sectors, petroleum/coal and computer and electronic products with most other sectors showing contraction.

That can hardly be termed "economic balance".

Now, if we wonder why the

manufacturing sector in the United States is failing, here is a graph that

may give us the answer:

Perhaps that explains why China now

finds that manufacturing now makes up 33.5 percent of its GDP compared to 22

percent in 1970.

I am hoping that all of this data

will make you realize that when you read headlines stating that the

"health" of the manufacturing sector in the United States is much

improved and that this factor will have an impact on tapering, that you will be able to

see that, despite the Federal Reserve's intervention since 2008, this once key sector of

the economy is on life support and is, unfortunately, relatively unimportant in

the grand scheme of what the Fed has planned for the future.

It would be interesting to see the total job numbers per capita for each sector (gains and losses). I've been wondering if our shift to high tech and resource extraction is making up for the losses to all other sectors i.e. are we balanced? This may provide a glimpse how healthy our model of borrow and spend really is.

ReplyDeleteThis whole tapering of bond purchases being tied to the health of the economy just raises questions for me though:

1 - with tapering, is the likely outcome not an eventual rise in interest rates?

2 - with rising interest rates, would the masses begin failing to cough up their debts?

3 - does the Fed know this and are they worried of the eventual outcome on their manipulation of liquidity?