Updated March 21, 2018

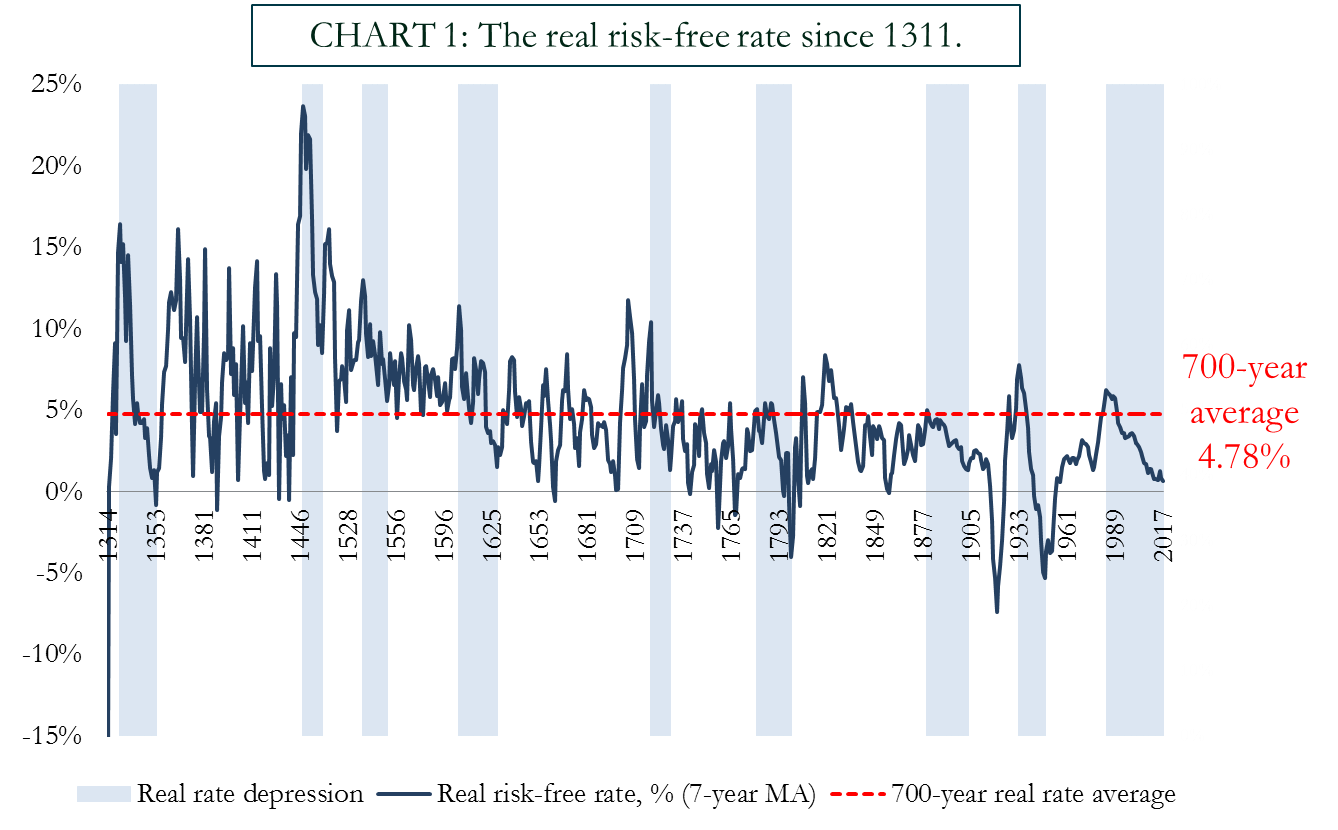

There is no doubt that we live in "interesting times" when it comes to global interest rates. For most of us, the post-Great Recession period of near zero interest rates has been unprecedented and the recent experiments with negative interest rates are a new reality for investors. While all of this may appear to be a brand new phenomenon, in fact, things are even more interesting when one looks at real interest rates, rates that are corrected for inflation as shown here:

There is no doubt that we live in "interesting times" when it comes to global interest rates. For most of us, the post-Great Recession period of near zero interest rates has been unprecedented and the recent experiments with negative interest rates are a new reality for investors. While all of this may appear to be a brand new phenomenon, in fact, things are even more interesting when one looks at real interest rates, rates that are corrected for inflation as shown here:

A recent

posting by Paul Schmelzing on the Bank of England's

"Bankunderground" blog looks at the really long term trends in real

interest rates and how, by putting the current interest rate environment into a

long-term context, we can better understand the relationship between the

current low real interest rate environment and the prospect for a return to "normal" interest rates. To assist with this relationship, the author has

looked at seven centuries of data for real risk free interest rates and has

produced this

graphic:

For your illumination, the source

of the risk-free asset data is as follows:

1.) 14th and 15th centuries -

sovereign rates in the Italian city states

2.) long-term rates in Spain

3.) long-term rates in the Province

of Holland

4.) long-term rates in the United

Kingdom after 1703

5.) long-term rates in Germany

6.) long-term rates in the United

States

From this data, the all-time real

average risk-free rate stands at 4.78 percent and the 200 year average stands

at 2.6 percent. As you can see from the red line on the previous graph,

the current rate environment is significantly depressed.

For those of us that have been

paying attention to nominal interest rates over recent decades, we've noticed a

significant downward trend as shown on this graph showing the yield on ten-year

Treasuries:

The author's calculations show a

similar trend in real rates over the very long-run as shown on the red line here:

On a constant time trend, the red

line shows an average fall in interest rates of about 1.6 basis points per

year.

If we take a further look at the

multi-century trends, we find that real rates have been depressed below long

term averages several times in what are termed "real rate depression

cycles". Here is a graphic showing the nine historical periods of real

rate depression plotted by size of interest rate depression versus the duration

of that depression:

As you can see here,

while the current period of real rate depression is relatively small when

measured using the amount of interest rate decline, it is the second longest

period of real rate depression over the 700 years in the study.

Lastly, let's look at how these

real interest rate depressions reverse themselves:

As you can see, real rates rise

very rapidly after they reach their trough, climbing an average of 3.15

percentage points within the first 2 years after the interest rate trough is

reached.

A long look back at historical data

suggests that the current depressed real interest

rate environment is not unique. While no one can predict the timing,

history also shows that real interest rates are likely to reverse themselves

very quickly. This reversal will have a significant impact on investors,

particularly bond investors, who will see the value of their fixed income

portfolios "readjust" in what could be a very negative way.

Let's close with this

quote from Alan Greenspan:

"By any measure, real

long-term interest rates are much too low and therefore unsustainable...When

they move higher they are likely to move reasonably fast. We are experiencing a

bubble, not in stock prices but in bond prices. This is not discounted in the

marketplace.”

Caveat emptor.

{kind=link}

{kind=link}

For a long time, it has appeared the whole world is trapped in an easy money low-interest rate environment with no way out. This is a sign that in the future a massive problem is developing and it holds huge economic ramifications and a major risk.

ReplyDeleteMany of us have a problem lending hard earned money out for a long period of time and we should be wary. Rates are based on predictions of future government deficits and events around the world that may or may not unfold as expected.

If the bond market is indeed a bubble the implications of its collapse will be massive and such an event will not only affect bondholders but will test the economic foundations of both the country and the world. Bond holders would be stripped of wealth and soaring interest rates will magnify the nations debt service and rapidly impact our deficit. More on this subject in the article below.

http://brucewilds.blogspot.com/2015/12/bond-market-bubble-ending-has-massive.html

So What? Nothing but mental masterbation here. If rates go up, governments will DEFAULT, period. This will lead to WWIII in earnest. Is that what you are really predicting? LOL!

ReplyDelete