Thanks to the Federal Reserve and its central bank peers, the

world is now awash in debt. This is particularly the case in the

corporate sector where debt has been accrued to record levels, an issue that is

of concern, particularly when one of two scenarios play out; a rise in interest

rates or a slowing of the economy. In the most recent version of theInternational Monetary Fund's Global Financial Stability Report for April 2017,

the IMF takes a detailed look at the global corporate sector debt levels and

expresses concerns over the worsening debt serviceability issues. In this posting, we'll look at the debt situation

for the corporate sectors in both the United States and take a brief look at the corporate debt situation in the world's emerging economies.

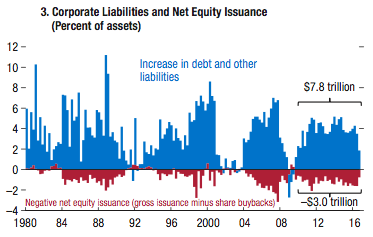

The IMF begins by noting

that the U.S. corporate sector has added $7.8 trillion in debt and other

liabilities since 2010 with traditional equity financing being outstripped by

share buybacks as you can see here:

Here is a graphic

showing how the net leverage (ratio of net debt to EBITDA or earnings before income tax, depreciation and amortization) for big corporations

in the United States:

As you can see, median

corporate leverage among large corporations has grown steadily since the end of

the Great Recession and is now close to historically high levels at 1.5 times

earnings.

Here is a graphic

showing net leverage for key sectors of the economy, comparing the level in

2004 to 2006 to the level in 2016:

Eight out of ten sectors

showed an increase in leverage with only two showing a decrease over the

decade; industrials and real estate, although the net debt of these three sectors is still very high.

Here is a graphic

showing the debt service burden (red line) for the American corporate sector:

Despite the current ultra-low

interest rate environment, the debt service burden for Corporate America has

risen substantially since 2015.

Here is a graphic

showing interest rate coverage ratios (ratio of EBIT (earnings before income tax) to interest payments):

As you can see, higher

interest rates could push the interest rate coverage ratio downwards even further, significantly weakening the ability of corporations to cover

interest owing on their debt.

Here is a graphic

showing the percentage of firms at risk of default:

At 22.1 percent, the

percentage of firms that are at risk of default is at the highest level since

the turn of the millennium.

Now, let's take a brief look at the corporate sector debt situation in the world's emerging market economies. Here is a graphic

showing which nations have corporate debt that is at risk (i.e. interest

coverage ratio of less than 1) should global trade decline, economic growth

decrease and protectionist trade pressures rise:

Corporations in nations

that rely heavily on manufacturing and commodity exports are particularly

vulnerable to increases in debt risk since they are the economies that will be

impacted the most by protectionism as shown here:

As we can see from this

report, thanks to the current ultra-low interest rate fantasy land, the

corporate sector in both the United States and the world's emerging market economies is highly vulnerable to changes in interest rates, largely because it has

gorged itself at the cheap debt trough. Earnings have dropped to less than six

time interest expense, a level that is close to the lowest levels seen during

the Great Recession. While many of these troubled firms are in the

beleaguered energy sector, firms in both the real estate and utilities sector

are showing debt pressures as well. Under a scenario where there is a

sharp rise in interest rates, the IMF projects that the combined assets of debt

challenged American firms could reach almost $4 trillion, a scenario that does

not bode well for investors, particularly those that have invested in high

yield corporate debt.

No comments:

Post a Comment