A recent speech by the General Manager of the Bank for International Settlements or BIS at the International Center for Monetary and Banking Studies gives us insight into where the central bank of central banks feels that the economy is heading. This information is particularly pertinent given that governments and some central bankers have been insisting that inflationary pressures are merely transient and that prices increases will settle down over the short-term.

Let's start by looking at a brief video of Agustin Carstens from October 2020 so that we can get a sense of where his sentiments lie:

Frightening, isn't it? But at least now we know his agenda.

Now, let's look at some key excerpts from his speech given on April 5, 2022 with my bolds throughout:

"After more than a decade of struggling to bring inflation up to target, central banks now face the opposite problem. The shift in the inflationary environment has been remarkable. If you had asked me a year ago to lay out the key challenges for the global economy, I could have given you a long list, but high inflation would not have made the cut.

This evening, I will describe the rise in inflation over the past year and discuss why this came as a surprise to many. I will argue that the pandemic and the extraordinary policy response laid the groundwork for a rapid and goods-intensive bounceback in demand which supply has been unable to fully meet. The war in Ukraine has further disrupted supply, particularly for commodities. I will also draw some broader lessons about the inflationary process – in particular, the need to look “under the hood” of aggregate data and models to understand how the behaviour of individual firms and workers drives inflation outcomes.

A key message is that we may be on the cusp of a new inflationary era. The forces behind high inflation could persist for some time. New pressures are emerging, not least from labour markets, as workers look to make up for inflation-induced reductions in real income. And the structural factors that have kept inflation low in recent decades may wane as globalisation retreats."

In other words, central bankers don't have a clue about what lies ahead for the economy.

Here is a graphic from the presentation showing how the global economy is entering a new reality that has not been experienced for four decades:

Carstens notes that 60 percent of the world's advanced economies have experienced year-over-year inflation above 5 percent which is more than 3 percentage points above the 2 percent target set by many central banks. He also notes that inflation has been rising in the world's emerging markets with more than half experiencing inflation rates that are above 7 percent.

Let's continue with his musings:

"At first, in early 2021, price increases were confined to a small number of items. Energy, food and durable goods, such as cars, are the most familiar examples. We tend to think of these as relative price changes resulting from shifts in demand and supply, many pandemic-induced. The items where supply and demand imbalances were concentrated had relatively flexible prices, allowing quick adjustments. Indeed, for a while it was possible to attribute all of the increase in inflation to these items, making it look transitory.

But higher inflation has become increasingly broad based. Since the start of 2021, the share of items in the consumption basket that have seen very large price rises has increased steadily. In particular, growth in service prices has accelerated. Because growth in service prices tends to be more persistent than that in goods, inflation may be becoming more entrenched."

Here is a graphic showing how inflation has broadened over time for both advanced and emerging economies:

Now, let's look at the three reasons why he believes that inflation has risen:

1.) The strong global rebound in aggregate demand: the global economy is expanding much more quickly than in the post-recession recoveries of recent decades.

2.) A persistent rotation in demand towards goods and away from services, particularly customer-facing ones. This trend has continued with supply growth being unresponsive to the higher demand. Staggered lockdowns and disrupted global value chains have revealed the fragility of the global "just-in-time" manufacturing systems.

3.) unresponsive aggregate supply, which has found it hard to keep up with surging demand.

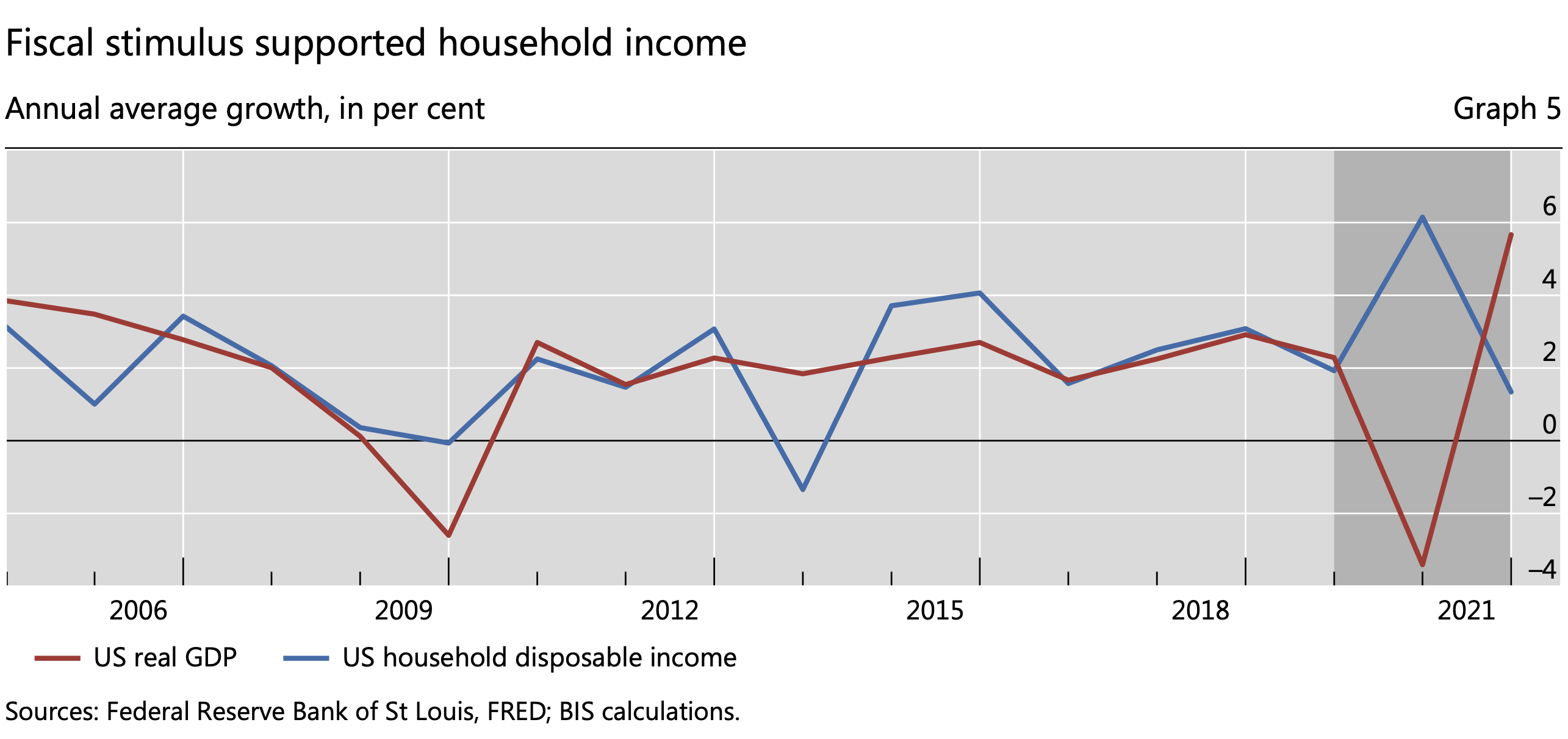

He states that the recovery from the pandemic was "remarkably fast", largely because economic activity was artificially repressed by government responses to the pandemic (i.e. lockdowns). It was the "exceptional policy response" that is responsible for this because governments used fiscal stimulus to support demand and central banks used monetary policies (i.e. expanding the supply of money) both of which have served as a springboard for the rapid post-pandemic economic expansion over the past year in particular. Here is a graphic showing how fiscal stimulus supported household disposable income:

Here, to me, is the key to the inflation dilemma, at least in the United States:

All of that new money has to have somewhere to go.

Carstens notes the following two lessons that need to be learned:

1.) "The distinction between relative price changes and inflation is critical, but not always clear-cut. In hindsight, it was too tempting to dismiss the initial rises in energy, food and car prices as a one-off adjustment to changed demand. We have learned once more that sector-specific shocks can spill into other sectors and become more persistent and pervasive.

This can happen directly or indirectly, through rising input costs that percolate down the value chain. Indeed, recent bottlenecks have been so keenly felt partly because they occurred in items at the start of production chains, which are needed to produce other goods and services downstream."

2.) "High- and low-inflation environments are very different. When inflation is high, price changes tend to be more aligned. Their common component explains a large share of the total variability of individual price changes. By contrast, in an environment of low and stable inflation, as in the last two decades, price changes in individual items – even large ones – percolate less into the prices of other items and, therefore, aggregate price indices. Put differently, when inflation is persistently low, much of what we measure as inflation is, in fact, the result of idiosyncratic price changes.

A consequence of this is that low-inflation environments tend to be largely self-correcting. Large price rises in individual items can increase inflation for a while. But if other prices don’t respond, inflation will eventually come down.

When inflation is less persistent, its influence on wage- and price-setting loses traction."

So, where to from here? Carstens notes that measures of long-term inflation have increased as shown here as projected by economic forecasters, financial markets and households:

One concern is that some households' inflation expectations have risen a lot and if that tendency spreads, central bankers will find it much harder to bring inflation back down. As well, as inflation starts to affect the cost of living, it is increasingly likely that a dangerous wage-price spiral could develop as consumers develop a mindset that they need significant wage increases to keep pace with price increases.

Here are Carstens' final comments:

"The good news is that central banks are awake to the risks. No one wants to repeat the 1970s. It seems clear that policy rates need to rise to levels that are more appropriate for the higher- inflation environment. Most likely, this will require real interest rates to rise above neutral levels for a time in order to moderate demand.

The adjustment to higher interest rates will not be easy. In many countries, starting conditions complicate matters. Households, firms, financial markets and sovereigns have become too used to low interest rates and accommodative financial conditions, also reflected in historically high levels of private and public debt. It will be a challenge to engineer a transition to more normal levels and, in the process, set realistic expectations of what monetary policy can deliver.

Nor will the required shift in central bank behaviour be popular. But central banks have been here before. They are fully aware that the short-term costs in terms of activity and employment are the price to pay to avoid bigger costs down the road. And such costs represent an investment in central banks’ precious credibility, which yields even longer-term benefits.

The shifts do underscore that central banks cannot single-handedly ensure global growth by keeping an accommodative stance in all conditions. Amid low inflation, this perception became commonplace. It is one central banks must continue to fight against, even more so in an inflationary environment."

In other words, get used to higher interest rates. They are coming whether we like it or not and the resulting pain for highly indebted consumers among the serf class is going to be substantial. We have been lulled into believing that the near-zero interest rate environment was permanent and have consumed with this as our reality. But, on the upside, the central bankers living among the sweaty masses will never have to worry about being unemployed no matter how pitiful the accuracy of their economic prognostications turn out.

In conclusion and as an aside, I found it particularly interesting/concerning that Agustin Carstens used the word "surprise" (or a derivation of the word) ten times throughout this brief speech. Doesn't that tell us everything that we need to know about central bankers and their understanding of the economy?

No comments:

Post a Comment